This Industry Viewpoint was contributed by Michael Quinn & Jordan Rupar of Q Advisors

Q Advisors recently joined hundreds of leaders from across the cloud and managed services space at Cavell’s third annual European VoIP Summit in London. Industry consolidation was a recurring theme throughout the conference’s keynote speeches and discussion panels. With two large industry players, West Corporation and 8×8, “exploring strategic alternatives”, service providers are anticipating how the next wave of industry consolidation will impact the cloud and managed services space.

M&A and Investment Activity Outlook

At the European VoIP Summit in London, Q Advisors presented their insights on the M&A environment and the growing wave of consolidation in the cloud and managed services space. There are several broad economic factors fueling heightened M&A activity; namely, buyers leveraging strong balance sheets, a low interest rate environment, and cash-rich consolidators. On a narrower market view, increased deal activity is being driven by several other industry-specific factors including:

- Global IT Service and Cloud Companies are seeking transformative acquisitions aimed at achieving several strategic outcomes. These include entering new lines of business, penetrating new geographic regions, acquiring core technology platforms and solutions, and acquiring mid-to-large customer bases.

- Traditional Telecom Providers are continuing to augment existing solutions through M&A. They have renewed efforts to attract SMEs and large enterprises by upselling cloud-based managed services. Telcos are also actively pursuing bolt-on acquisitions aimed at new cloud products and solutions, customer bases, and expanding their geographic reach, particularly into Europe.

- Private Equity Firms continue to invest in the cloud managed services sector.

While PE firms prefer to back businesses with contracted, recurring revenue models, they will fund the transformation of legacy telecom revenues to cloud recurring models. Several PEs are also looking to build up newly acquired cloud platforms, which will drive a second wave of M&A activity over the next

24 months.

Market Impact of New Entrants

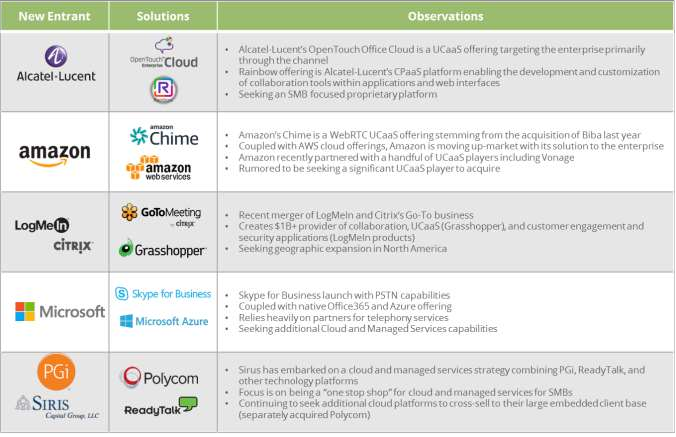

In addition to the “usual suspects,” there are many new entrants actively exploring the cloud and managed services market through M&A and organic efforts. These players are expected to have a profound impact on near-term cloud M&A activity as well as the makeup of future cloud solution bundles. Several of these new entrants are large cloud technology providers (i.e., Amazon and Cisco) that have traditionally served SMEs with tangential solutions such as cloud infrastructure services or communications equipment.

These players are looking to move up the stack in much the same way Microsoft has done with Skype for Business. They are focusing on developing an integrated enterprise cloud offering, where their traditional offerings are paired with more innovative cloud offerings such as cloud UC, contact center, and managed security solutions. The chart below identifies

new entrants, their products, and provides key observations on the next wave of cloud and managed services acquirers.

Several of these new entrants will be among the next wave of consolidators in the cloud and managed services space. In addition to telecom and technology companies, the next wave of consolidators will include cloud infrastructure players such as Amazon and Google, SaaS vendors such as Oracle and Salesforce, hosting providers like GoDaddy, and value- added resellers such as Insight and Ingram Micro. These players are likely to buy one of the cloud pure plays in the space rather than build their own platform or solution, given their abundant cash positions and the speed to market of a buy vs. build approach.

Running to Where the Ball is Going

M&A activity in the cloud and managed services space continues to accelerate as the adoption of these services has become more accepted across the SME and geographic landscapes. Countries where cloud penetration has been extremely low, such as Germany, are starting to see a tremendous uptick in acceptance rates. The enterprise segment of the market has also crossed the adoption transom.

Given this ever-expanding marketplace and the desire of SMEs to have “one throat to choke” for all solutions, new market entrants with deep pockets are entering the arena and taking advantage of their significant customer bases, where they can upsell new solutions and services. Those smaller market players that offer a single cloud service or solution are likely to find themselves in a gun fight with only a knife if they do not become part of a larger multi-solution enterprise.

In the words of professional soccer player Johan Cruff, “There’s only one moment in which you can arrive in time. If you’re not there, you’re either too early or too late.” Service providers must run to where the ball is going, rather to where it has been, in the fast-evolving cloud managed services space. Service providers can stay ahead of the game by focusing on the following areas of differentiation, which include the ability to (1) move up the services stack, (2) offer multiple innovative services (i.e., more tools in the toolbox), (3) achieve geographic diversification, (4) demonstrate vertical expertise, (5) exemplify their role as a trusted advisor, and (6) achieve scale either organically or through M&A.

Michael Quinn / Partner

Michael Quinn, founding partner of Q Advisors, brings a unique and highly valuable background to telecom, media, and technology (TMT) investment banking that combines finance, hands on M&A experience, and law. With more than 25 years of international operations and investment banking experience in the telecommunications industry, Michael has originated, structured, and executed more than 100 deals totaling more than $4 billion in transaction value. Michael’s deep industry expertise and extensive transaction experience has enabled him to lead M&A and debt and equity financings in a variety of TMT sectors including cloud and managed services, competitive wireline telecom, wireless, digital media, social networking, mobile content, satellite and mobile infrastructure and solutions. He has led transactions for Q Advisors’ clients including: Arkadin, Atlantic Tele-Network, Inc., Broadcore, BroadSmart, Grande Communications, Hudson Fiber, Magnetic North, Masergy Communications, Neverblue, One Source Networks, and TelePacific. Michael brings to the table a reputation as a creative problem solver; passionately committed to obtaining the optimal results for the firm’s clients.

Prior to forming Q Advisors, Michael was a founder of and Chief Corporate Development Officer for VeloCom Inc., a Latin American wireless services provider, where he was responsible for capital raising and acquisition activities. Michael began his career with the New York-based law firm of Cleary, Gottlieb, Steen & Hamilton. He later became a partner in the Denver-based law firm Holland & Hart LLP, guiding their international corporate finance practice.

Jordan Rupar / Vice President

Jordan Rupar joined Q Advisors in 2012. She has executed numerous mergers and acquisitions, equity financings and strategic advisory assignments for clients across the telecom, media, and technology (TMT) industries with a particularly deep focus on cloud communications, software and technology, IoT, and other emerging growth sectors. Specific clients on whose transactions she has been engaged include: ANPI, Arkadin, Broadsmart, Calligo, CallTower, Magnetic North, One Source Networks, Telesphere Networks, UNSi and

WennSoft.

About Q Advisors

Q Advisors LLC (www.qllc.com) is a world-class global boutique investment bank formed in 2001 serving public and private companies, PE firms, entrepreneurs and large multi-nationals in the telecom, media, and technology (TMT) sectors. The firm has extensive, global reach, while also providing the personalized service of a boutique advisory firm. Thanks to our partners and senior staff, who come from leading investment banks and operating companies, we leverage extensive industry knowledge and analytical insights to help our clients achieve successful M&A and capital markets transactions.

If you haven't already, please take our Reader Survey! Just 3 questions to help us better understand who is reading Telecom Ramblings so we can serve you better!

Categories: Cloud Computing · Industry Viewpoint · Managed Services · Mergers and Acquisitions · Unified Communications · VoIP

Discuss this Post