In a surprise holiday announcement that has turned my earlier review of the 2012 US fiber M&A market into premature ramblings, Lightower Fiber Networks and Sidera Networks announced this morning their intention to merge. Berkshire Partners is behind the deal, in which both companies will be acquired for some $2B and then merged under the leadership of current Lightower CEO Rob Shanahan.

ABRY Partners, which has owned Sidera for several years now, and Pamlico Capital, which is one of Lightower’s major owners, will remain as investors in the combined company alongside Berkshire. The ownership status of other private equity groups that had a piece of either company (M/C Partners, Ridgemont Equity Partners, Spectrum Equity Investors) after the deal was not specified, but one must expect that at least several have decided to cash out. ABRY and Berkshire are of course very familiar with each other, as they currently jointly own Telx as well.

Last month I took this look at the northeastern US fiber M&A situation, describing it as ‘unresolved’ with three major regional/metro footprints owned by private equity jockeying for position: Lightower, Sidera and Fibertech. I have long had the sense that at least some of the money guys behind them would eventually decide to team up and pool their assets for a better competitive position. I am pleased to have been right for once!

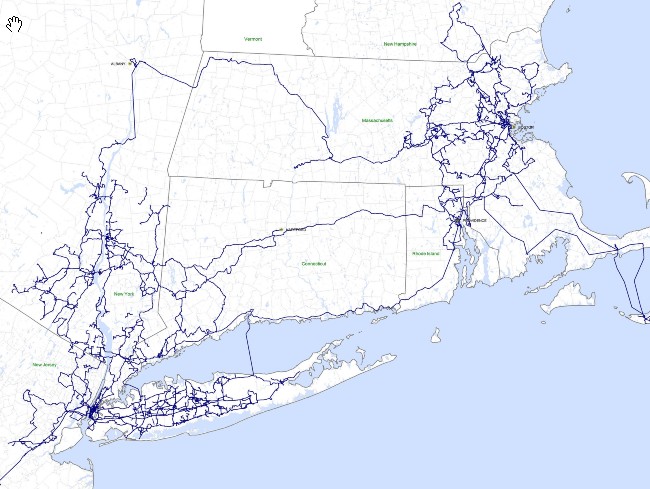

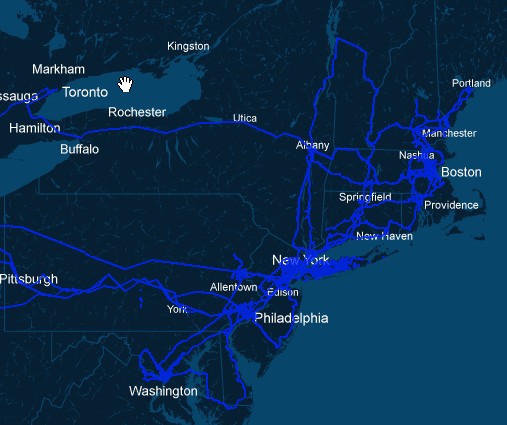

The synergies are obvious, as the combined company will have one of the most extensive fiber footprints available along the northeastern corridor, reaching more than 6,000 on-net buildings. Their footprints are very complementary, with Lightower’s metro extent in Massachussetts and the Hudson River valley matching well with Sidera’s somewhat more centralized depth in each city. Meanwhile, Sidera’s metro assets in Tier III/IV markets elsewhere gets come company as well. Here is a look at their overall maps side by side.

|

|

Both companies were active consolidators over the past five years, but have been quiet for the past year on that front. Lightower’s inorganic activity has included the acquisitions of KeySpan, DataNet, Lexent, Veroxity, and Open Access, as well as a deal for NStar’s remaining capacity. Sidera’s footprint derives from those of RCN, ConEd Communications, Neon, and the Long Island Fiber Exchange.

It stands to reason that the combined company and its active private equity backers will be on the lookout for further M&A to further improve its competitive position regionally. That could mean assets in Pennsylvania, Upstate NY, Maryland, or even out in Ohio/Indiana or to the south in Virginia and the Carolinas. But it should be noted that they surely had the chance to move on Litecast or First Communications, but Zayo won those auctions earlier this quarter. An eventual merger with Zayo looks strategically very possible someday, with an exit for all these private equity guys available via one big IPO or something.

Further details on the transaction were not disclosed, but they expect to close the deal in the second quarter of 2013.

If you haven't already, please take our Reader Survey! Just 3 questions to help us better understand who is reading Telecom Ramblings so we can serve you better!

Categories: Mergers and Acquisitions · Metro fiber

Very interesting. I’ve always considered these two carriers to be the best options for TWTC to pick up and complete their footprint in these regions. Either it becomes even sweeter now to bid on the combined assets & show they want to go toe to toe with zayo/L3… or they’ve just blown yet another opportunity to show they are in it for the long haul and not a sell out.

Why wouldn’t CenturyLink be interested in these assets?

It’s always possible, but if they do make a move then tw telecom seems like a better fit.

I’ve always thought along similar lines. The counter-argument is that both Sidera and Lightower tend to have a more wholesale approach than tw telecom so the fit is less exact than it might otherwise be.

i thought 2 billion to be a very large buyout for a regional players albeit in the Northeast. Zayo picked up Abovenet, AFS,AGL etc combined for less then that. That is a big $$ ticket to get in the northeast8 game. Fibertech must be very happy with there position at this point

The $2B figure does raise eyebrows, but it’s unclear yet just what the breakdown there is. Perhaps more details will filter out.

I still believe that Fibertech represents a tremendous opportunity from an M&A perspective in the Northeast. The amount of services under contract, the extensive fiber and the profitability is attractive. When does Dan Caruso pick up the next obvious piece?

Can anyone comment on why CenturyLink/Qwest is not on this site’s list of major fiber-optic carriers? My understanding was that the old Qwest was a major long-haul builder and carrier, so it should have had substantial assets for CL to have acquired. Perhaps these were sold off prior to the acquisition of Q by CL.

Thank you.

Which list are you referring to?

Different question Rob, when (or are they already) will the KDL/PAETEC/WIN maps be combined?